Buyers seem to be feeling more confident in taking on variable rate mortgages, and I believe that 2023 presents a good window of opportunity to engage in a much more calmer home search and buying experience following the intense market conditions of the last few years as we see things rebound into Summer and fall 2023

I reviewed the 2023 First Quarter Housing Forecast by the British Columbia Real Estate Association (BCREA). According to the report, the slowing economy and still elevated mortgage rates are expected to keep housing activity lower than usual throughout the first half of 2023

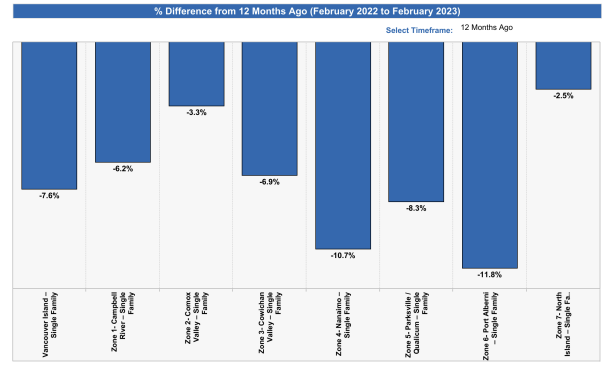

In terms of benchmark prices (MLS® Home Price Index), the board-wide benchmark price for a single-family home in February 2023 was $732,500. This represents an eight percent decrease from one year ago.

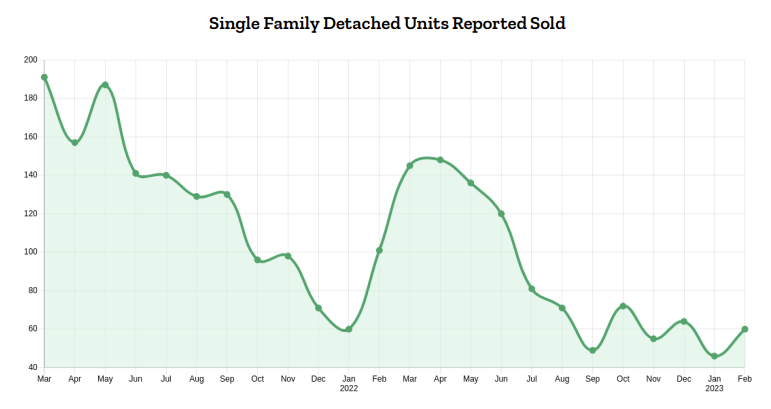

The below graph represents the Nanaimo Area market for single family homes.

The recent trends in the national and provincial Real Estate market could impact our local market. Vancouver Island’s attractiveness as a destination for buyers from other areas could increase competition, making it more challenging for locals to find suitable properties.

I observed that 220 single-family homes were sold, marking a 37% decrease from one year ago when 350 homes were sold. However, there was a 33% increase from January 2023 when 165 homes were sold. In the same month, condo apartment sales stood at 64 units, a 40% decrease year over year, but a 52% increase from the previous month. On the other hand, row/townhouse sales were at 50 units, a 44% drop from one year ago and a 39% increase from January.

Despite the increase in inventory, the market is still below the ideal level for a balanced market.

In conclusion, although there has been an increase in listings compared to the beginning of 2022, inventory levels are still low compared to historical levels. As a result, we do not expect supply to normalize until sometime in 2026. This weak inventory will put more pressure on prices when demand increases.

Area Breakdown

|

Area |

Price of Single-family Home |

Year Over Year Change |

|

Campbell River |

$652,600 |

-6% |

|

Comox Valley |

$789,600 |

-3% |

|

Cowichan Valley |

$738,200 |

-7% |

|

Nanaimo |

$750,500 |

-11% |

|

Parksville-Qualicum |

$848,100 |

-8$ |

|

Port Alberni |

$516,500 |

-12% |

|

North Island |

$414,700 |

-3% |

Canadian Outlook

Across Canada we still have an inventory and affordability issue with an additional 3.5M affordable housing units are needed by 2030

Around 2003 and 2004, an household on average income would have had to devote close to:

- 40% of their disposable income to buy an average house in Ontario

- 45% of their disposable income to buy an average house in British Columbia.

In 2021, a household on average income would have had to devote close to 60% of their incomes to housing

I have been monitoring the recent market data, and it’s worth noting that the impacts seen in the larger market do have an effect on our region as well. In particular, we have many buyers from other areas moving to Vancouver Island, and the trends observed in the national and provincial Real Estate market affect our local market.

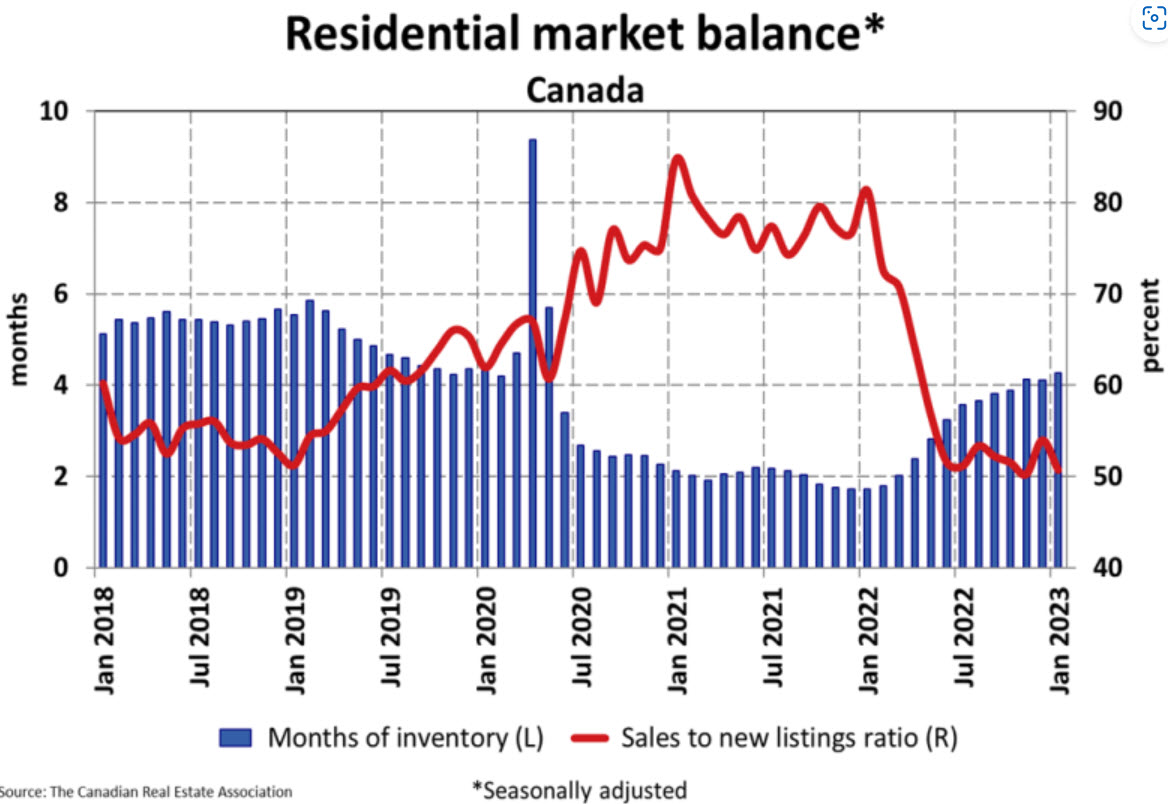

In January, the number of newly listed homes increased by 3.3% on a month-over-month basis, led by increases across British Columbia. However, despite this small increase, new listings remain historically low on a national level, with January 2023 marking the lowest level for that month since 2000. This shortage of new supply could impact the local market and lead to increased competition among buyers.

As new listings increased and sales decreased in January, the sales-to-new listings ratio eased back to 50.7%, which is roughly where it had been over the entire second half of 2022. This measure’s long-term average is 55.1%. The low sales-to-new listings ratio could suggest that the demand for properties remains high, which could lead to continued price growth in the region.

On a national basis, there were 4.3 months of inventory at the end of January 2023, which is similar to the level leading up to the initial COVID-19 pandemic lockdowns and still about a month below the long-term average of about five months. This low inventory level could also impact the local market, making it challenging for buyers to find available properties.

The Aggregate Composite MLS® Home Price Index (HPI) showed a 1.9% decline on a month-over-month basis in January 2023, continuing the trend that began last spring. The HPI now sits 15% below its peak level, which was reached in February 2022. Prices across the country have decreased from peak levels more in many parts of Ontario and some parts of British Columbia, and less in other areas. However, Calgary, Regina, Saskatoon, and St. John’s stand out as markets where home prices are barely off their peaks at all.

Interest Rates

The Bank of Canada has maintained its target for the overnight lending rate at 4.5% after eight successive rate hikes and continues its policy of quantitative tightening. The Bank reported global economic developments aligning with their expectations amid slowing global growth and easing inflationary pressures, with China’s economic recovery and the Russia-Ukraine war as key sources of upside risk. Overall financial conditions have tightened in recent months, with the Canadian dollar losing value against its U.S. counterpart.

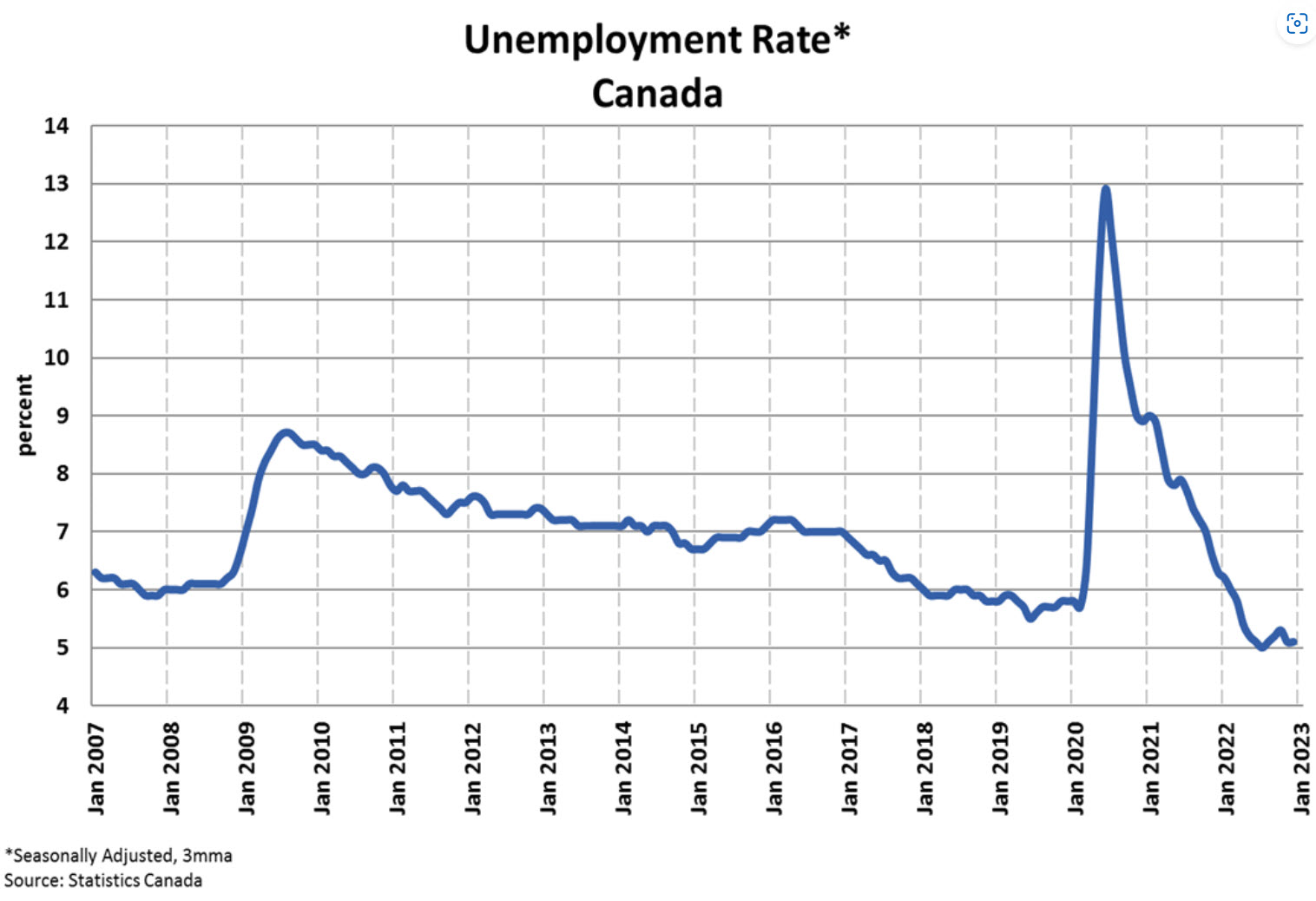

Fourth quarter economic growth in Canada was flat, coming in below expectations, mainly due to a falloff in inventory investment. Tight monetary policy continues to weigh on household spending and business investment amidst slowing domestic and foreign demand. However, the labour market remains vibrant, as evidenced by strong job gains, low unemployment, increased job vacancies, and wage growth of 4-5%.

Inflation

According to recent reports from the Bank, global inflation remains high and broad-based, but it is starting to retreat in many countries due to lower energy prices and supply chain improvements. Although financial conditions have eased in recent months, they continue to be restrictive, and the Canadian dollar remains stable relative to the US dollar.

The Canadian economy has shown stronger growth than initially anticipated, despite excess demand and a tight labour market. However, the restrictive monetary policy is contributing to a slowdown in economic activity, as evidenced by the recent decline in household spending and a significant decrease in the housing market activity. Furthermore, rising interest rates are expected to negatively impact business investments, while weaker foreign demand will likely dampen exports.

2023 Q1 Market Intelligence Report

The Bank estimates that the Canadian economy grew by 3.6% in 2022. Looking ahead, GDP growth is expected to slow to about 1% in 2023, followed by a slightly stronger pace of growth of around 2% in 2024.

Although inflation has eased in the second half of 2022, declining from 8.1% in June to 6.3% in December, food and shelter costs continue to rise, causing hardships for many Canadians. Despite short-term inflation expectations remaining elevated, recent data suggests that core inflation has probably peaked, as evidenced by the decline in the 3-month measures of core inflation.

Overall, the Bank projects a significant pullback in CPI inflation this year, expected to come in at around 3% by mid-2023, with a further retreat to the Bank’s 2% target by 2024. Lower energy prices, supply chain improvements, and rising interest rates are expected to be the primary contributing factors to lower inflation this year and next.

In conclusion, despite the challenges faced by the housing market in the current economic climate, the market intelligence report predicts a strong recovery in the near future. This prediction is based on the expected decline in mortgage rates and record-high immigration, which are expected to provide momentum for the housing market in 2024. As always, it is important for industry professionals to stay informed and vigilant in order to make the most of the opportunities presented by these market conditions and to always look at your property independently from the general market cycle.