We aim to provide you with valuable insights to help you navigate the current real estate landscape.

Sales and Listings Statistics

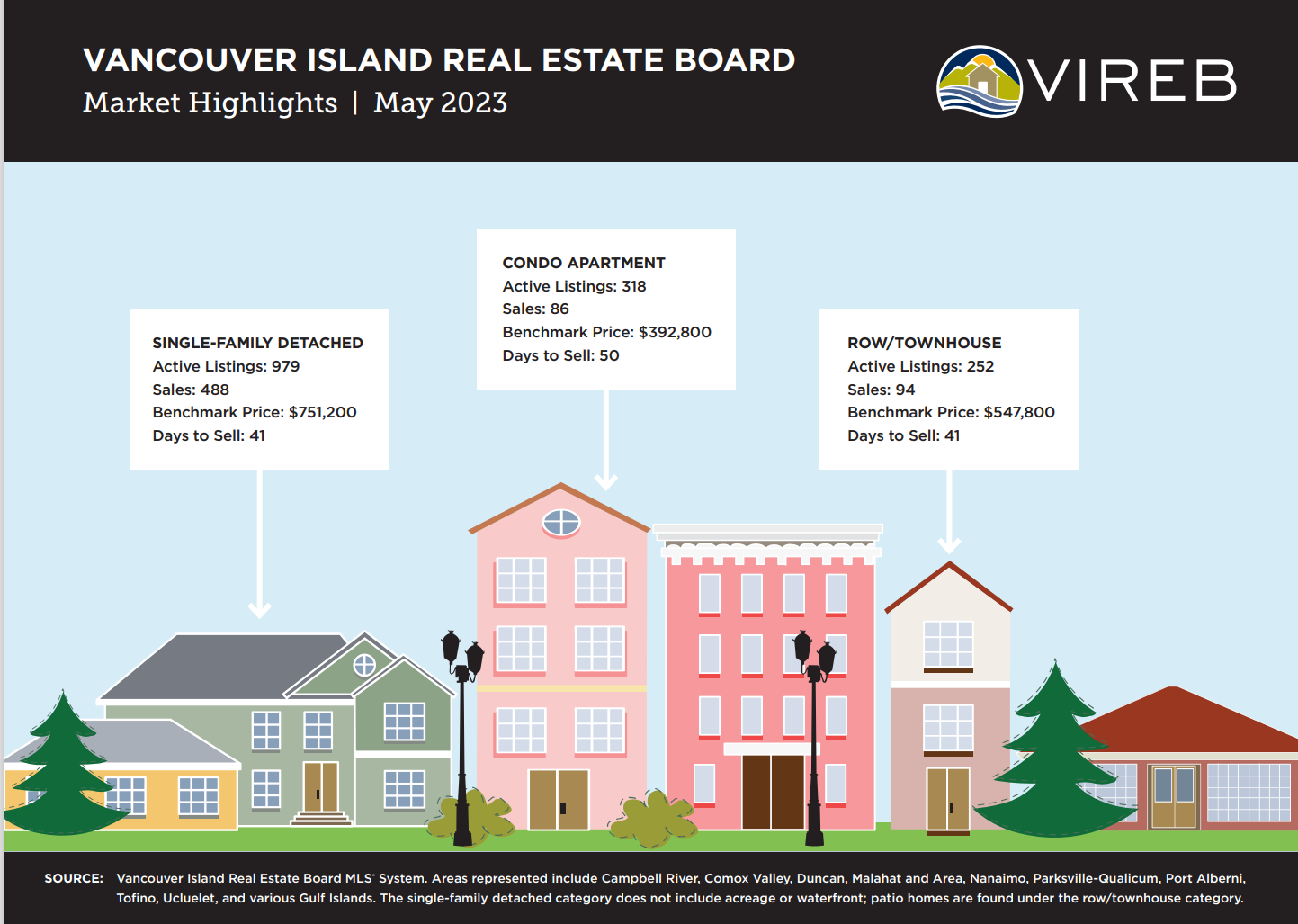

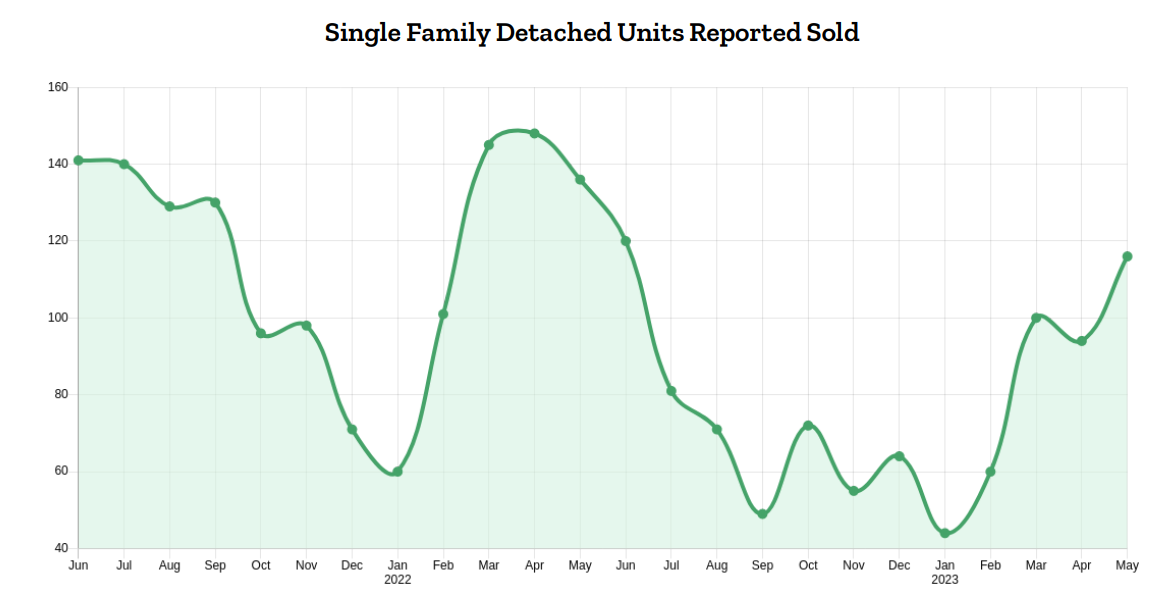

Single-Family Homes in Nanaimo: There were 488 sales in May 2023, representing an 8% increase compared to the previous year and a significant 25% increase from April 2023.

Table: Sales and Listings Statistics

Sales Performance:

Single-Family Homes: There were 979 active listings in May, slightly higher than the previous year’s 976 listings.

Buyers and sellers are taking a more measured approach, resulting in smart pricing and measured offers.

Benchmark Prices (MLS® Home Price Index):

Find out more about the current market on our YouTube channel https://www.youtube.com/@bchomes